Technical

What is a Master Trust?

Oct 07, 2022

Technical

Offering life benefits requires an employer to set up a registered pension scheme or excepted discretionary trust to pay benefits. Many employers are comfortable doing this themselves but for those without the time, expertise or size, an insurer’s Master Trust could be an option where the employer is insuring the life benefits.

A Master Trust is a discretionary trust capable of providing benefits to a range of different employers unconnected to each other. Each employer operates within its own segregated section of the insurer’s Master Trust, with the trustees taking care of the administration and the legal and tax responsibilities.

This video explores what a Master Trust is and how it supports organisations who offer group life benefits.

Setting up and administering a company-owned trust can be time-consuming. As well as appointing a trustee, employers need to understand tax law and ensure they comply with HMRC rules and reporting requirements.

A Master Trust provides a flexible and tax-effective approach. The employer can choose the group life assurance cover they want for the business but the legal responsibility, decision-making and tax reporting is all taken care of by the Master Trust’s independent trustee.

Employers who want to offer life cover without the burden of administering their own trust, can join an insurer’s Master Trust.

This is a readymade discretionary trust set up and managed by an independent trustee appointed by the insurer.

Think of it like a filing cabinet. The filing cabinet itself is the discretionary trust with each of the files the individual employers who use the master trust.

They have their own policy specific to their needs, but all of the trust administration and reporting is carried out by the trustee.

In the event of a claim, the insurer will assess eligibility and pay any benefit to the trustee. The trustee will then look at any expression of wish form that may have been completed by the deceased employee to help determine the appropriate beneficiaries and distribute the money accordingly.

Using a Master Trust is convenient. Setting up a trust can take time, potentially putting the group life policy on hold until everything’s in place. With a Master Trust, it’s all set up and ready to go.

As well as saving an employer time, and a potential headache sorting out the administration and reporting requirements, it’s usually free to join an insurer’s Master Trust.

There’s usually nothing to pay to join and usually no fees for reporting or for dealing with benefits paid to the trust following a claim.

Any employer can join their Group Life insurer’s Master Trust. All they need to do is hold a group life policy with the insurer and complete the process to join the Master Trust.

This involves completing an employer admission form, which is provided by the insurer. This asks for information including employer name; registered office or principal place of business; contact names and details; organisation type and Companies House number.

It’s also possible for an employer to take advantage of the Master Trust structure if they offer, or want to offer, registered and excepted benefits.

As registered and excepted benefits have different tax treatments, the employer will need to take out separate group life policies and complete an admission form for each Master Trust.

Although a Master Trust can take care of all of an employer’s responsibilities around setting up and running a group life trust, there are some potential issues to consider.

In particular, if the employer switches to a different insurer for their group life arrangement, they will also need to set up a new trust arrangement. It may be possible to use the new insurer’s Master Trust for the new policy, but, if they don’t offer one, the employer may need to set up their own trust.

Neither is a Master Trust always the most appropriate option for an employer. If they already have trustees in place to look after the company pension scheme, another option is to extend their duties to the group life arrangement too.

But, for those employers who might baulk at the thought of establishing their own trust, a Master Trust can be a good solution. Everything is taken care of by the professional trustees, leaving the employer free to focus on running their own business.

A Master Trust is governed by a constitution set out in its trust deeds and rules. This will stipulate the responsibilities of the trustees, the group life insurer and the Master Trust members.

The trustee – or trustees – of a Master Trust are independent of the group life insurance provider. They may be a legal firm or a provider of trustee services with experience managing and administering trust arrangements.

An employer that currently uses its own registered pension scheme or excepted discretionary trust to pay group life benefits can move to its insurer’s Master Trust. It is sensible to take legal and tax advice if considering this as there may be ramifications for employees with enhanced or fixed protection.

If an employer switches to a different insurer for their group life arrangement, they will also need to set up a new trust arrangement. It may be possible to use the new insurer’s Master Trust for the new policy, but, if they don’t offer one, the employer may need to set up their own trust.

If an employer wishes to leave its group life insurer’s Master Trust, as it has set up its own scheme to provide benefits, it will need to notify the insurer, who will be able to advise them on the leaving process. This varies between Master Trusts but should be simple and straightforward.

A complicated corporate structure such as this should make no difference from a Master Trust perspective. All the employees of the principal employer and associated employers can be covered under one Master Trust.

Where there is a major change in the corporate structure, the new principal employer will need to speak to the group life insurer about whether it wants to remain in the Master Trust. Depending on its decision and the insurer’s Master Trust rules, this may require a new application to the Master Trust.

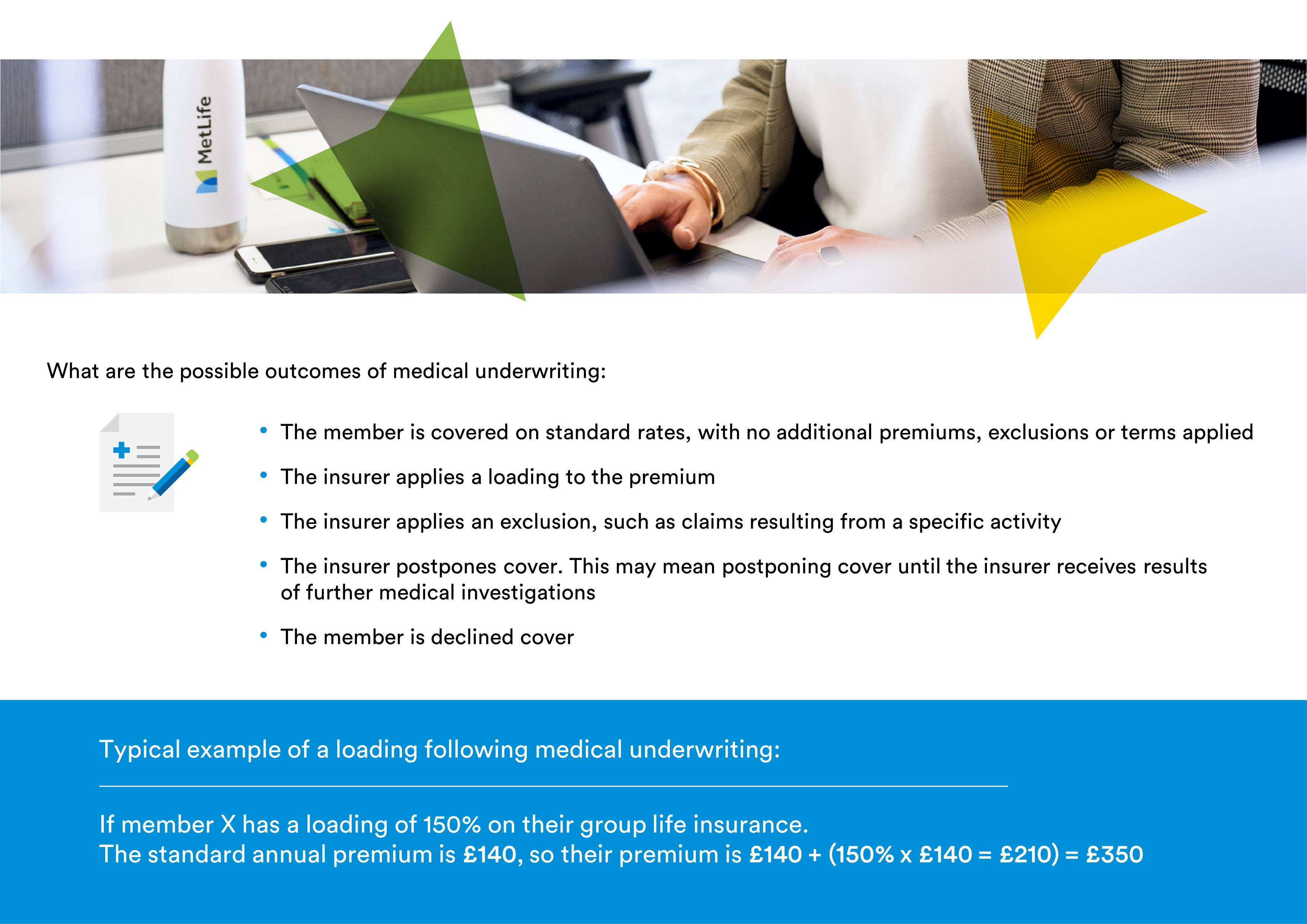

Medical underwriting can take time so the insurer will offer temporary cover while it is ongoing. This provides the member with the peace of mind that cover is in place if they did become unwell or die during the underwriting process.

To protect the insurer, a pre-existing condition exclusion is applied to this temporary cover. This excludes any claims that are the result of an existing condition from the last 5 years (for example). This does not need to have been diagnosed.

Temporary cover is usually in place for 90 days but it can be extended if an underwriting decision is still pending.

This depends. A forward underwriting bar may be applied at the point of underwriting. This grants some additional benefit to cover future increases, but a member may need to be medically underwritten again, depending on the terms.

For example, one insurer might offer a further 30% of benefit; another may apply the forward underwriting bar for two years, providing there are no benefit increases in excess of £100,000. If the member exceeds these terms, or a time period ends, they will need to be re-underwritten.

Another option is ‘OneStep’ underwriting where, providing there are no changes to the cover, members do not need to be underwritten again. At MetLife we offer this for policies of 20 members or more.

A one step underwriting bar of £5m is applied and providing the scheme doesn’t change cover and the member doesn’t exceed the £5m benefit increase, which is very unlikely, then there is no need for further medical underwriting.